Importo totale (1 articolo articoli):

Destinazione ordine:

mean variance analysis portfolio choice di markowitz harry (32 risultati)

Feedback

Vai alla pagina principale dei risultati di ricerca

Filtri di ricerca

Tipo di articolo

- Tutti i tipi di prodotto

- Libri (32)

- Riviste e Giornali (Nessun altro risultato corrispondente a questo perfezionamento)

- Fumetti (Nessun altro risultato corrispondente a questo perfezionamento)

- Spartiti (Nessun altro risultato corrispondente a questo perfezionamento)

- Arte, Stampe e Poster (Nessun altro risultato corrispondente a questo perfezionamento)

- Fotografie (Nessun altro risultato corrispondente a questo perfezionamento)

- Mappe (Nessun altro risultato corrispondente a questo perfezionamento)

- Manoscritti e Collezionismo cartaceo (Nessun altro risultato corrispondente a questo perfezionamento)

Condizioni

Legatura

Ulteriori caratteristiche

- Prima ed. (7)

- Copia autograf. (1)

- Sovracoperta (Nessun altro risultato corrispondente a questo perfezionamento)

- Con foto (7)

- Non Print on Demand (30)

Lingua (2)

Spedizione gratuita

- Spedizione gratuita in Italia (Nessun altro risultato corrispondente a questo perfezionamento)

Paese del venditore

Valutazione venditore

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets. With a chapter and program by G. Peter Todd

Editore: Frank J. Fabozzi Associates [John Wiley & Sons], New Hope, PA [Chichester], 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: Versand-Antiquariat Dr. Gregor Gumpert, Berlin, Germania

Valutazione del venditore 5 su 5 stelle

EUR 29,00

Convertire valutaEUR 16,00 per la spedizione da Germania a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloHardcover. Condizione: Gut. Gr. 8�. XIX u. 379 Seiten mit zahlreichen graphischen Darstellungen (�berwiegend Diagramme), Papp-Bd. - Die erste Ausgabe des Werks ist 1987 erschienen. Die vorliegende Ausgabe aus dem Jahr 2000 ist erweitert um ein dreizehntes Kapitel (von G. Peter Todd), ein Vorwort von William F. Sharpe und ein 'Preface to Revised Reissue' des Autors. Mit Literaturangaben und Index. - Der Einband leicht berieben. Im unteren Bereich des R�ckdeckels R�ckst�nde eines Klebeetiketts.

-

Mean Variance Analysis in Portfolio Choice and Capital Markets

Editore: Wiley & Sons, Incorporated, John, 1987

ISBN 10: 0631153810 ISBN 13: 9780631153818

Lingua: Inglese

Da: Better World Books, Mishawaka, IN, U.S.A.

Valutazione del venditore 5 su 5 stelle

Prima edizione

EUR 29,21

Convertire valutaEUR 18,40 per la spedizione da U.S.A. a ItaliaQuantit�: 2 disponibili

Aggiungi al carrelloCondizione: Good. First Edition. Former library book; may include library markings. Used book that is in clean, average condition without any missing pages.

-

Mean Variance Analysis in Portfolio Choice and Capital Markets

Editore: Wiley & Sons, Incorporated, John, 1987

ISBN 10: 0631153810 ISBN 13: 9780631153818

Lingua: Inglese

Da: Better World Books, Mishawaka, IN, U.S.A.

Valutazione del venditore 5 su 5 stelle

Prima edizione

EUR 29,21

Convertire valutaEUR 18,40 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloCondizione: Good. First Edition. Used book that is in clean, average condition without any missing pages.

-

Mean-variance analysis in portfolio choice and capital markets. Ex-Library.

Editore: Frank J. Fabozzi Associates, (New Hope, Pennsylvania), 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: Yushodo Co., Ltd., Fuefuki-shi, Yamanashi Pref., Giappone

Membro dell'associazione: ILAB

Valutazione del venditore 5 su 5 stelle

EUR 48,61

Convertire valutaEUR 13,36 per la spedizione da Giappone a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloHardcover. Condizione: Good. xix, 379 p., Rev. reissue with new Chapter 13.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: GreatBookPrices, Columbia, MD, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 62,69

Convertire valutaEUR 17,80 per la spedizione da U.S.A. a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: As New. Unread book in perfect condition.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: GreatBookPrices, Columbia, MD, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 69,56

Convertire valutaEUR 17,80 per la spedizione da U.S.A. a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: GreatBookPricesUK, Woodford Green, Regno Unito

Valutazione del venditore 5 su 5 stelle

EUR 69,94

Convertire valutaEUR 17,94 per la spedizione da Regno Unito a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Editore: Somerset, New Jersey, U.S.A.: John Wiley & Sons Inc, 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: Bingo Books 2, Vancouver, WA, U.S.A.

Valutazione del venditore 4 su 5 stelle

EUR 58,24

Convertire valutaEUR 31,16 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloHardcover. Condizione: Near Fine. hardback book in near fine condition.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: Ria Christie Collections, Uxbridge, Regno Unito

Valutazione del venditore 5 su 5 stelle

EUR 82,54

Convertire valutaEUR 10,75 per la spedizione da Regno Unito a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New. In.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Editore: Frank J. Fabozzi Associates, 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: THE SAINT BOOKSTORE, Southport, Regno Unito

Valutazione del venditore 5 su 5 stelle

EUR 80,88

Convertire valutaEUR 12,40 per la spedizione da Regno Unito a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloHardback. Condizione: New. New copy - Usually dispatched within 4 working days. 735.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: SecondSale, Montgomery, IL, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 63,99

Convertire valutaEUR 31,16 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloCondizione: Very Good. Item in very good condition! Textbooks may not include supplemental items i.e. CDs, access codes etc.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: SecondSale, Montgomery, IL, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 63,99

Convertire valutaEUR 31,16 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloCondizione: Good. Item in good condition. Textbooks may not include supplemental items i.e. CDs, access codes etc.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: Griffin Books, Stamford, CT, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 59,61

Convertire valutaEUR 35,62 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrellohardcover. Condizione: As New. Looks new and unread but has ownership ink to flyleaf. A23 Please email for photos. Larger books or sets may require additional shipping charges. Books sent via US Postal.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: California Books, Miami, FL, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 88,96

Convertire valutaEUR 8,01 per la spedizione da U.S.A. a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: Majestic Books, Hounslow, Regno Unito

Valutazione del venditore 5 su 5 stelle

EUR 91,63

Convertire valutaEUR 10,58 per la spedizione da Regno Unito a ItaliaQuantit�: 3 disponibili

Aggiungi al carrelloCondizione: New. pp. 400.

-

EUR 90,07

Convertire valutaEUR 9,70 per la spedizione da Germania a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloGebunden. Condizione: New. Über den AutorrnrnnHarry M. Markowitz is president of Harry Markowitz Co. in San Diego. In 1990, he was jointly awarded the Nobel Prize for economics with Merton Miller and William Sharpe. nKlappentextIn 1952, .

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: Books Puddle, New York, NY, U.S.A.

Valutazione del venditore 4 su 5 stelle

EUR 103,76

Convertire valutaEUR 8,01 per la spedizione da U.S.A. a ItaliaQuantit�: 3 disponibili

Aggiungi al carrelloCondizione: New. pp. 400 1st Edition.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets (Hardcover)

Editore: John Wiley & Sons Inc, New York, 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: CitiRetail, Stevenage, Regno Unito

Valutazione del venditore 5 su 5 stelle

Prima edizione

EUR 78,19

Convertire valutaEUR 35,87 per la spedizione da Regno Unito a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloHardcover. Condizione: new. Hardcover. In 1952, Harry Markowitz published "Portfolio Selection," a paper which revolutionized modern investment theory and practice. The paper proposed that, in selecting investments, the investor should consider both expected return and variability of return on the portfolio as a whole. Portfolios that minimized variance for a given expected return were demonstrated to be the most efficient. Markowitz formulated the full solution of the general mean-variance efficient set problem in 1956 and presented it in the appendix to his 1959 book, Portfolio Selection. Though certain special cases of the general model have become widely known, both in academia and among managers of large institutional portfolios, the characteristics of the general solution were not presented in finance books for students at any level. And although the results of the general solution are used in a few advanced portfolio optimization programs, the solution to the general problem should not be seen merely as a computing procedure. It is a body of propositions and formulas concerning the shapes and properties of mean-variance efficient sets with implications for financial theory and practice beyond those of widely known cases. The purpose of the present book, originally published in 1987, is to present a comprehensive and accessible account of the general mean-variance portfolio analysis, and to illustrate its usefulness in the practice of portfolio management and the theory of capital markets. The portfolio selection program in Part IV of the 1987 edition has been updated and contains exercises and solutions. In 1952, Harry Markowitz published "Portfolio Selection," a paper which revolutionized modern investment theory and practice. The paper proposed that, in selecting investments, the investor should consider both expected return and variability of return on the portfolio as a whole. Portfolios that minimized variance for a given expected return were demonstrated to be the most efficient. Markowitz formulated the full solution of the general mean-variance efficient set problem in 1956 and presented it in the appendix to his 1959 book, Portfolio Selection. Though certain special cases of the general model have become widely known, both in academia and among managers of large institutional portfolios, the characteristics of the general solution were not presented in finance books for students at any level. And although the results of the general solution are used in a few advanced portfolio optimization programs, the solution to the general problem should not be seen merely as a computing procedure. It is a body of propositions and formulas concerning the shapes and properties of mean-variance efficient sets with implications for financial theory and practice beyond those of widely known cases. The purpose of the present book, originally published in 1987, is to present a comprehensive and accessible account of the general mean-variance portfolio analysis, and to illustrate its usefulness in the practice of portfolio management and the theory of capital markets. The portfolio selection program in Part IV of the 1987 edition has been updated and contains exercises and solutions. Shipping may be from our UK warehouse or from our Australian or US warehouses, depending on stock availability.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: GreatBookPricesUK, Woodford Green, Regno Unito

Valutazione del venditore 5 su 5 stelle

EUR 98,08

Convertire valutaEUR 17,94 per la spedizione da Regno Unito a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: As New. Unread book in perfect condition.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets (Frank J. Fabozzi Series)

Da: Revaluation Books, Exeter, Regno Unito

Valutazione del venditore 5 su 5 stelle

EUR 110,36

Convertire valutaEUR 11,96 per la spedizione da Regno Unito a ItaliaQuantit�: 2 disponibili

Aggiungi al carrelloHardcover. Condizione: Brand New. 1st edition. 399 pages. 9.00x6.00x1.25 inches. In Stock.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets (Hardcover)

Editore: John Wiley & Sons Inc, New York, 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: AussieBookSeller, Truganina, VIC, Australia

Valutazione del venditore 3 su 5 stelle

Prima edizione

EUR 92,69

Convertire valutaEUR 32,95 per la spedizione da Australia a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloHardcover. Condizione: new. Hardcover. In 1952, Harry Markowitz published "Portfolio Selection," a paper which revolutionized modern investment theory and practice. The paper proposed that, in selecting investments, the investor should consider both expected return and variability of return on the portfolio as a whole. Portfolios that minimized variance for a given expected return were demonstrated to be the most efficient. Markowitz formulated the full solution of the general mean-variance efficient set problem in 1956 and presented it in the appendix to his 1959 book, Portfolio Selection. Though certain special cases of the general model have become widely known, both in academia and among managers of large institutional portfolios, the characteristics of the general solution were not presented in finance books for students at any level. And although the results of the general solution are used in a few advanced portfolio optimization programs, the solution to the general problem should not be seen merely as a computing procedure. It is a body of propositions and formulas concerning the shapes and properties of mean-variance efficient sets with implications for financial theory and practice beyond those of widely known cases. The purpose of the present book, originally published in 1987, is to present a comprehensive and accessible account of the general mean-variance portfolio analysis, and to illustrate its usefulness in the practice of portfolio management and the theory of capital markets. The portfolio selection program in Part IV of the 1987 edition has been updated and contains exercises and solutions. In 1952, Harry Markowitz published "Portfolio Selection," a paper which revolutionized modern investment theory and practice. The paper proposed that, in selecting investments, the investor should consider both expected return and variability of return on the portfolio as a whole. Portfolios that minimized variance for a given expected return were demonstrated to be the most efficient. Markowitz formulated the full solution of the general mean-variance efficient set problem in 1956 and presented it in the appendix to his 1959 book, Portfolio Selection. Though certain special cases of the general model have become widely known, both in academia and among managers of large institutional portfolios, the characteristics of the general solution were not presented in finance books for students at any level. And although the results of the general solution are used in a few advanced portfolio optimization programs, the solution to the general problem should not be seen merely as a computing procedure. It is a body of propositions and formulas concerning the shapes and properties of mean-variance efficient sets with implications for financial theory and practice beyond those of widely known cases. The purpose of the present book, originally published in 1987, is to present a comprehensive and accessible account of the general mean-variance portfolio analysis, and to illustrate its usefulness in the practice of portfolio management and the theory of capital markets. The portfolio selection program in Part IV of the 1987 edition has been updated and contains exercises and solutions. Shipping may be from our Sydney, NSW warehouse or from our UK or US warehouse, depending on stock availability.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: BennettBooksLtd, North Las Vegas, NV, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 95,15

Convertire valutaEUR 39,18 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrellohardcover. Condizione: New. In shrink wrap. Looks like an interesting title!

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: Lakeside Books, Benton Harbor, MI, U.S.A.

Valutazione del venditore 4 su 5 stelle

EUR 68,33

Convertire valutaEUR 66,78 per la spedizione da U.S.A. a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New. Brand New! Not Overstocks or Low Quality Book Club Editions! Direct From the Publisher! We're not a giant, faceless warehouse organization! We're a small town bookstore that loves books and loves it's customers! Buy from Lakeside Books!

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: 3rd St. Books, Lees Summit, MO, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 110,06

Convertire valutaEUR 26,71 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloSoft cover. Condizione: Very Good. Very good, clean, tight condition. Text free of marks. Professional book dealer since 1999. All orders are processed promptly and carefully packaged.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Da: Lucky's Textbooks, Dallas, TX, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 72,44

Convertire valutaEUR 66,78 per la spedizione da U.S.A. a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets (Hardcover)

Editore: John Wiley & Sons Inc, New York, 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: Grand Eagle Retail, Fairfield, OH, U.S.A.

Valutazione del venditore 5 su 5 stelle

Prima edizione

EUR 85,64

Convertire valutaEUR 66,78 per la spedizione da U.S.A. a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloHardcover. Condizione: new. Hardcover. In 1952, Harry Markowitz published "Portfolio Selection," a paper which revolutionized modern investment theory and practice. The paper proposed that, in selecting investments, the investor should consider both expected return and variability of return on the portfolio as a whole. Portfolios that minimized variance for a given expected return were demonstrated to be the most efficient. Markowitz formulated the full solution of the general mean-variance efficient set problem in 1956 and presented it in the appendix to his 1959 book, Portfolio Selection. Though certain special cases of the general model have become widely known, both in academia and among managers of large institutional portfolios, the characteristics of the general solution were not presented in finance books for students at any level. And although the results of the general solution are used in a few advanced portfolio optimization programs, the solution to the general problem should not be seen merely as a computing procedure. It is a body of propositions and formulas concerning the shapes and properties of mean-variance efficient sets with implications for financial theory and practice beyond those of widely known cases. The purpose of the present book, originally published in 1987, is to present a comprehensive and accessible account of the general mean-variance portfolio analysis, and to illustrate its usefulness in the practice of portfolio management and the theory of capital markets. The portfolio selection program in Part IV of the 1987 edition has been updated and contains exercises and solutions. In 1952, Harry Markowitz published "Portfolio Selection," a paper which revolutionized modern investment theory and practice. The paper proposed that, in selecting investments, the investor should consider both expected return and variability of return on the portfolio as a whole. Portfolios that minimized variance for a given expected return were demonstrated to be the most efficient. Markowitz formulated the full solution of the general mean-variance efficient set problem in 1956 and presented it in the appendix to his 1959 book, Portfolio Selection. Though certain special cases of the general model have become widely known, both in academia and among managers of large institutional portfolios, the characteristics of the general solution were not presented in finance books for students at any level. And although the results of the general solution are used in a few advanced portfolio optimization programs, the solution to the general problem should not be seen merely as a computing procedure. It is a body of propositions and formulas concerning the shapes and properties of mean-variance efficient sets with implications for financial theory and practice beyond those of widely known cases. The purpose of the present book, originally published in 1987, is to present a comprehensive and accessible account of the general mean-variance portfolio analysis, and to illustrate its usefulness in the practice of portfolio management and the theory of capital markets. The portfolio selection program in Part IV of the 1987 edition has been updated and contains exercises and solutions. Shipping may be from multiple locations in the US or from the UK, depending on stock availability.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Editore: Frank J. Fabozzi Associates, 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: Kennys Bookshop and Art Galleries Ltd., Galway, GY, Irlanda

Valutazione del venditore 5 su 5 stelle

Prima edizione

EUR 152,01

Convertire valutaEUR 2,00 per la spedizione da Irlanda a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New. 2000. 1st Edition. Hardcover. Num Pages: 700 pages, black & white illustrations. BIC Classification: KF. Category: (UF) Further/Higher Education; (XV) Technical / Manuals. Dimension: 228 x 157 x 26. Weight in Grams: 705. . . . . .

-

EUR 133,55

Convertire valutaEUR 29,89 per la spedizione da Regno Unito a ItaliaQuantit�: 1 disponibili

Aggiungi al carrellopaperback. Condizione: Good. Good. book.

-

Mean-Variance Analysis in Portfolio Choice and Capital Markets

Editore: Frank J. Fabozzi Associates, 2000

ISBN 10: 1883249759 ISBN 13: 9781883249755

Lingua: Inglese

Da: Kennys Bookstore, Olney, MD, U.S.A.

Valutazione del venditore 5 su 5 stelle

EUR 191,16

Convertire valutaEUR 1,96 per la spedizione da U.S.A. a ItaliaQuantit�: Pi� di 20 disponibili

Aggiungi al carrelloCondizione: New. 2000. 1st Edition. Hardcover. Num Pages: 700 pages, black & white illustrations. BIC Classification: KF. Category: (UF) Further/Higher Education; (XV) Technical / Manuals. Dimension: 228 x 157 x 26. Weight in Grams: 705. . . . . . Books ship from the US and Ireland.

-

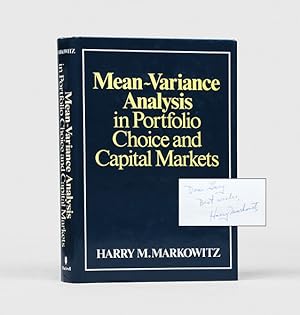

Mean-Variance Analysis in Portfolio Choice and Capital Markets.

Editore: Oxford: Basil Blackwell, 1987, 1987

Da: Peter Harrington. ABA/ ILAB., London, Regno Unito

Membro dell'associazione: ABA ILAB PBFA

Valutazione del venditore 5 su 5 stelle

Prima edizione Copia autografata

EUR 1.170,07

Convertire valutaEUR 11,96 per la spedizione da Regno Unito a ItaliaQuantit�: 1 disponibili

Aggiungi al carrelloFirst edition, first impression, presentation copy, inscribed on the title page: "Dear Gary: Best Wishes, Harry Markowitz". Here, Markowitz (1927-2023) outlines a consciously accessible account of his method of portfolio analysis, while underlining its usefulness for professional investment management. Markowitz jointly won the Nobel Prize for Economics in 1990 for his work on portfolio theories and stock market risk. Octavo. Tables and graphs in the text. Original dark blue boards, spine lettered in gilt. With dust jacket. Minimal bumping to spine ends; slight rubbing and creasing to unclipped jacket: a near-fine copy in like jacket.